The backlog of applications for federal student loan forgiveness is ballooning—despite growing urgency and mounting frustration from borrowers. The Department of Education is still unable to make meaningful progress, leaving many applicants stuck in limbo.Forbes

The mess began with rapid policy shifts—courts halted programs like SAVE, forcing abrupt freezes on processing. These legal roadblocks, combined with sudden changes like program shutdowns, have thrown systems into disarray.Student Loan PlannerInvestopedia

Income-Driven Repayment (IDR) Processing: Over 1.5 million IDR applications are lingering unprocessed. A chunk of those are being denied outright because borrowers applied for blocked plans or defaulted to “lowest payment” options that are no longer available.Student Loan PlannerInvestopediaMarketWatch

PSLF Buyback Program: Those hoping to reclaim months of non-qualifying payments to qualify for Public Service Loan Forgiveness face growing delays. Backlogs have surged from around 49,000 to over 65,000 in just a couple of months.Student Loan PlannerInvestopedia

The backlog ripples across the system:

Borrower Complaints: The Department of Education’s ombudsman and feedback offices are buried—handling tens of thousands of unresolved cases.Student Loan PlannerThe Times of India

Rising Defaults: As of mid-2025, 5.6 million borrowers were officially in default—and that number could near 10 million by year-end.Student Loan Planner

Staffing Shortfalls: Massive layoffs (~40–50%) at the Education Department and Federal Student Aid (FSA) have decimated institutional knowledge and slowed resolution times across the board.The Washington PostReutersThe New YorkerThe Times of India

Borrowers are left scrambling, unsure if they’ll ever receive relief. For many, every month counts—and delays could mean mounting interest, missed deadlines, or even default. The system designed to offer options and relief is now a maze of chaos and delay.

Issue | Status & Impact |

|---|---|

IDR Applications | 1.5 million pending; many denied—especially those tied to halted plans. |

PSLF Buyback Requests | Backlog soared to over 65,000, despite some processing. |

Borrower Complaints | Tens of thousands of unresolved cases clogging ombudsman and feedback channels. |

Defaults Rising | 5.6M borrowers currently in default; potentially close to 10M by end of year. |

Staff Cuts | Nearly half of FSA workforce slashed—crushing the department’s operational capacity. |

Reapply for IDR Plans: If denied due to blocked plans like SAVE, reapply for open options like IBR or PAYE using the online system with IRS data retrieval to speed things up.Student Loan Planner

Monitor PSLF Status: If pursuing PSLF especially via buyback, keep your application status in check. Delays are widespread—track carefully.

Reach Out to Representatives: Congressional offices often have dedicated casework teams. Filing a case with your representative may nudge stalled applications forward.

Consider Alternatives: If eligible for public service forgiveness, switching to a viable IDR plan may help ensure your payments count toward forgiveness while the backlog clears.

The Trump administration has rolled out a transformative—and controversial—proposal to tighten eligibility for the Public Service Loan Forgiveness (PSLF) program. The changes would disqualify borrowers whose employers engage in what the Department of Education deems activities with a “substantial illegal purpose.”(Inside Higher Ed, Business Insider)

Borrowers working for local or nonprofit organizations could lose PSLF benefits if their employer is found involved in activities like aiding undocumented immigrants, supporting terrorism, providing gender-affirming care, or violating federal discrimination laws.(Inside Higher Ed, Business Insider)

The administration argues this revision helps ensure taxpayer money isn’t granted to employers operating outside lawful or public-interest boundaries.(Inside Higher Ed, Business Insider)

If finalized, this rule would overwrite one of the core principles of PSLF: focusing on an individual’s public service, not the employer’s ideology or affiliations.(Inside Higher Ed, Business Insider)

Advocates worry the definition of “illegal purpose” is vague—and politically motivated. It could destabilize essential public service roles and even jeopardize millions of existing borrowers.(Inside Higher Ed, Business Insider, AP News, The Economic Times, The Times of India)

The proposed rule is open for public feedback now through September 17, 2025.(Inside Higher Ed, Business Insider)

If approved, it takes effect on July 1, 2026—but importantly, existing PSLF credits earned prior to that date remain intact.(Inside Higher Ed, Business Insider)

“This feels like government overreach… organizations and groups that are not working in line with the administration’s agenda are going to be targeted.”

— Sabrina Calazans, Student Debt Crisis Center(Inside Higher Ed)

Betsy Mayotte—the sole dissenting advisor on the rulemaking panel—warns the changes could chill public service and force employees to abandon jobs in hospitals or public defense.(Inside Higher Ed)

Emmanuel Guillory of the American Council on Education argues the proposal departs from Congress’s original intent to support individuals—not penalize them for their employers’ positions.(Inside Higher Ed)

| Aspect | Details |

|---|---|

| What’s being proposed? | Disqualifying PSLF eligibility for borrowers whose employers engage in certain “illegal” activities. |

| Who is affected? | Public servants like teachers, nurses, social workers—especially in organizations involved in sensitive social issues. |

| Why now? | Trump’s March 2025 executive order directed this rule change; it’s now published for public comment. |

| Timeline | Comments open through Sept 17, 2025; if adopted, rule kicks in July 1, 2026. Past credit remains safe. |

| Main concerns | Vague and potentially politicized criteria; could undermine recruitment in public sector; possible legal challenges. |

Submit a public comment before September 17—it’s your chance to influence the final rule.

Stay informed—track legal developments and advocacy efforts pushing back against the proposal.

For current PSLF borrowers: Keep an eye on updates from loan servicers and consider consulting experts for guidance.

Let me know if you’d like help drafting a public comment, understanding your current PSLF status, or exploring advocacy groups working on this issue.

2025 has been one of the most turbulent years in student loan history. Between the repeal of the SAVE Plan, the launch of the Repayment Assistance Plan (RAP), and renewed legal battles over debt cancellation, borrowers are left asking the same question:

Will student loan forgiveness still be here after 2025?

The answer is complicated. Forgiveness programs like PSLF and IDR forgiveness are still in place—but political shifts and budget constraints mean nothing is guaranteed.

In this article, we’ll break down:

The current state of federal forgiveness programs

How politics and lawsuits could reshape them

What borrowers can do now to protect their progress toward forgiveness

Despite the noise, several major forgiveness programs are still active:

Public Service Loan Forgiveness (PSLF) – Forgives remaining balance after 120 qualifying payments for eligible public service workers.

Income-Driven Repayment (IDR) Forgiveness – Forgives remaining balance after 20–25 years on an eligible IDR plan (now RAP, IBR, PAYE).

Teacher Loan Forgiveness – Offers $5,000–$17,500 for certain teachers after five years in a qualifying school.

📌 Full details: Federal Forgiveness Programs Overview

There are three main threats to forgiveness beyond 2025:

The 2024 elections shifted control of Congress, with key lawmakers openly critical of large-scale debt relief. Budget proposals for 2026 already include reduced allocations for forgiveness subsidies.

Multiple lawsuits are challenging both PSLF expansions and IDR reforms, arguing they exceed Department of Education authority.

Example: In early 2025, a coalition of states filed suit to block the One-Time Account Adjustment’s full implementation.

The Congressional Budget Office estimates forgiveness programs will cost over $550 billion in the next decade, creating pressure for reform or caps.

Borrowers have experienced major shifts:

SAVE Plan repeal – Removing the most generous interest subsidy in federal history.

RAP plan introduction – Payments based on 12% of discretionary income (higher than SAVE’s 10%).

Stricter PSLF employer verification – Annual submission is now mandatory, with real-time audits.

Here’s what analysts and policy experts say might be next:

Higher minimum payment requirements

Longer timelines for IDR forgiveness (e.g., 25 years minimum for all)

Caps on forgiven amounts (e.g., $50k max)

Possible elimination of PSLF for new borrowers

Parent PLUS loans excluded from IDR forgiveness entirely

More forgiveness for specific professions (healthcare, teaching, first responders)

Geographic incentives—loan relief tied to working in underserved regions

If you’re aiming for forgiveness, take these steps before any policy changes:

✅ Verify Your Repayment Plan

Check if you’re on RAP, IBR, or PAYE and whether it qualifies for forgiveness.

✅ Submit Employment Certification

If pursuing PSLF, file your PSLF Form every year without fail.

✅ Track Your Forgiveness Progress

Download your payment history from your loan servicer’s portal.

✅ Consolidate Non-Direct Loans

FFEL and Perkins loans must be consolidated into Direct Loans to count toward PSLF or IDR forgiveness.

📌 Guide: How to Protect Your Forgiveness Eligibility

Policy analysts suggest:

PSLF is likely to remain for current borrowers, but eligibility for future borrowers could tighten.

IDR forgiveness will continue, but with reduced interest subsidies and potentially higher payment calculations.

New targeted forgiveness programs may emerge—offering relief for priority workers rather than blanket policies.

No matter where you stand politically, the reality is this:

Forgiveness programs are policies, not guarantees. They can change—or disappear—depending on leadership, budgets, and court rulings.

If you’re in a qualifying program now, lock in your eligibility:

File the right forms

Stay on qualifying repayment plans

Keep meticulous records

The future of forgiveness beyond 2025 is uncertain, but proactive borrowers can protect themselves from being left behind.

In 2025, navigating student loans is more complicated—and risky—than ever before. With policy rollbacks, new plans like RAP, and the repeal of SAVE, borrowers are making costly mistakes every single day.

Whether you’re new to repayment or have been managing loans for years, avoiding these top errors can save you thousands of dollars, protect your credit, and speed up forgiveness.

Let’s walk through the biggest federal student loan mistakes borrowers are making in 2025—and how to avoid them.

One of the most common and dangerous mistakes is assuming you’re still on the SAVE Plan. The reality?

✅ SAVE was repealed in early 2025 under the One Big Beautiful Bill (OBBB).

If you were on SAVE, you’ve now been automatically placed in the Repayment Assistance Plan (RAP) unless you proactively switched.

📌 Action Step: Check your current repayment plan at studentaid.gov to confirm where you stand.

Income-Driven Repayment (IDR) plans—including RAP, IBR, and PAYE—require annual income recertification.

Failure to do so results in:

A jump to the Standard Plan (higher payments)

Loss of progress toward forgiveness

Accrued interest capitalizing onto your principal

🗓️ In 2025, deadlines are stricter than ever—no more COVID-era extensions.

✅ Set reminders every 11 months and recertify early.

If you’re working toward PSLF, you must:

Submit the PSLF Employment Certification Form annually

Be on a qualifying IDR plan (RAP, IBR, PAYE—not ICR for most)

Work full-time for a qualified employer

🎯 Mistake: Not submitting proof of employment every year.

📌 PSLF Certification Form Link (Studentaid.gov)

Many older borrowers still hold FFEL or Perkins Loans, which are not eligible for most modern relief programs, including:

IDR forgiveness

PSLF

RAP

Unless you consolidate them into a Direct Consolidation Loan, you’re locked out of key benefits.

📌 Direct Consolidation Application

It’s tempting to skip over emails or letters from MOHELA, Aidvantage, or Nelnet—but these updates could contain:

Payment due dates

Plan changes

Missed recertification warnings

Default notices

In 2025, more borrowers are entering delinquency and default just because they didn’t open their mail.

📌 Pro tip: Log into your servicer’s portal monthly. Set alerts.

The new RAP plan doesn’t cap unpaid interest like SAVE did. That means:

Your balance can grow again

Interest may compound more aggressively

You’ll end up paying more over time

🎯 If you’re budgeting based on last year’s rules, it’s time for a reset.

📌 Use the Student Loan Simulator to see real-time monthly payment estimates.

Many borrowers assume they’ll qualify for:

IDR forgiveness in 20–25 years

PSLF after 10 years

One-Time Account Adjustment

But forgiveness isn’t automatic and has strict eligibility requirements.

🛑 Common Mistake:

Skipping annual income certification

Being in the wrong repayment plan

Not working full-time at a qualifying employer

📌 Bookmark the Student Loan Forgiveness Center for ongoing updates and eligibility checklists.

In 2025, TikTok and shady “debt relief” companies are preying on desperate borrowers with false promises of:

Instant loan forgiveness

One-time discharge programs

Guaranteed $0 payments

⚠️ These are often scams that charge fees for things you can do yourself for free.

✅ You never have to pay to apply for IDR or forgiveness.

📌 Report suspicious offers to: https://reportfraud.ftc.gov/

Parent PLUS loans have fewer relief options:

Not eligible for PSLF unless consolidated

Only IDR option is ICR, which has high payments and a 25-year term

🛑 Mistake: Not consolidating or thinking SAVE or RAP applies to Parent PLUS.

📌 Learn more: https://www.studentloan-gov.com/parent-plus-help

Student loan rules are constantly changing in 2025. If you’re confused, don’t go it alone.

✅ You can get free support:

From your loan servicer

Through nonprofit credit counselors

Ignoring problems leads to:

Late payments

Damaged credit

Loan default

📌 Take action early, even if your situation feels overwhelming.

In 2025, staying informed is your best financial defense. Student loans are more complex than ever, but with smart habits and up-to-date information, you can avoid disaster.

✅ Remember:

Check your repayment plan status regularly

Don’t assume you’re in the best option

Recertify your income on time

Be proactive—not reactive

Explore more guides, checklists, and tools at:

👉 www.studentloan-gov.com

Updated – Dec 10th 2024

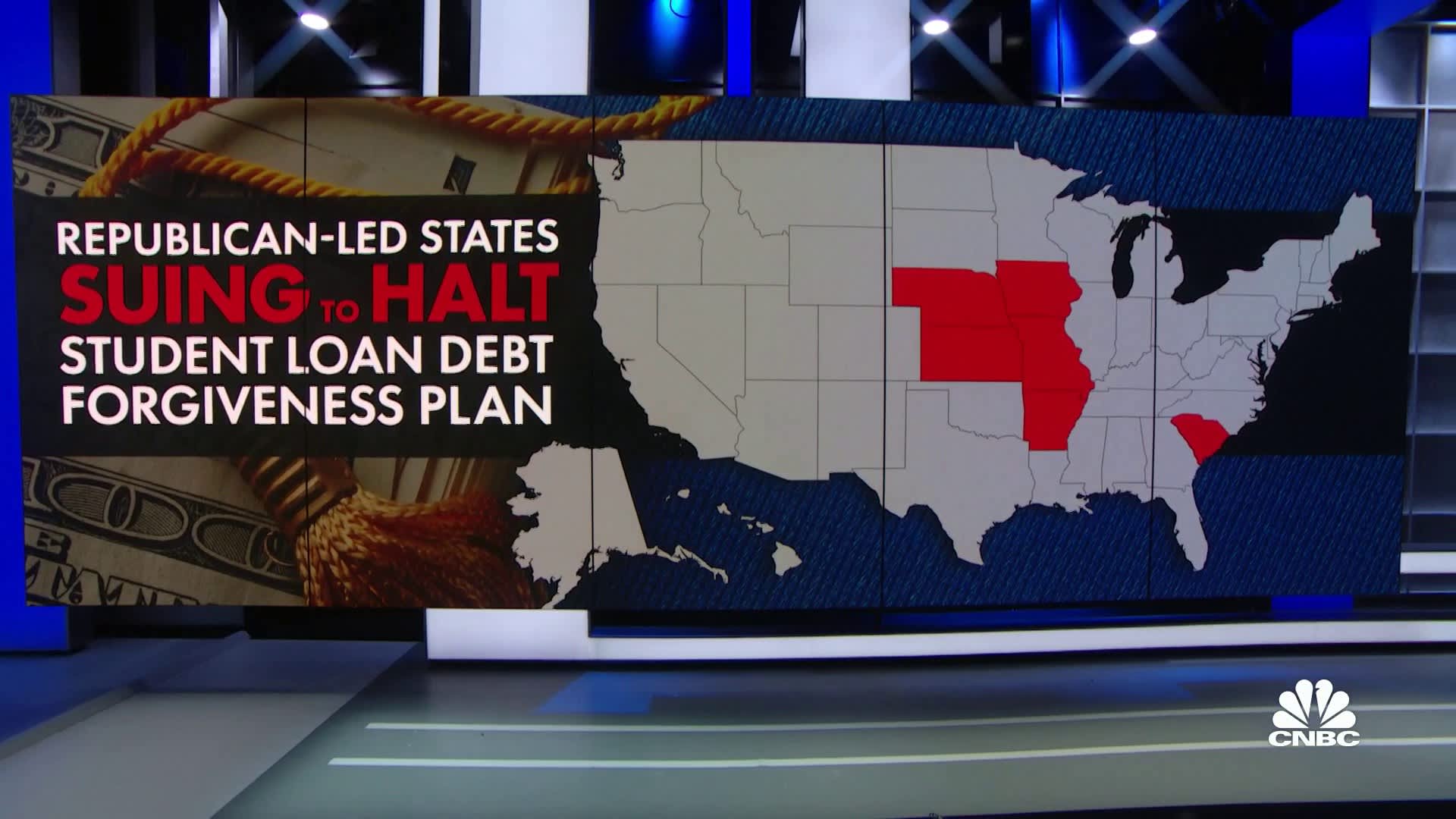

Last week a federal court put a temporary hold on the cancellation of federal student loans. Over 22 million borrowers have already applied for the Biden’s debt relief program.

The appeal was granted by the 8th circuit U.S. Courts of Appeals. The injunction was filed by a group of six republican states hoping to block the forgiveness program altogether.

The courts has not provided any information on when they will rule on the case. however it has been expedited on the motion. As of right now the courts has ordered the Biden administration to pause on canceling student loan debt under the program. Plans to start cancelling the debt was set to start as early as next week

The decision came a day after U.S. District Judge Henry E. Autrey, dismissed the states’ lawsuit for lack of standing. Earlier Thursday, U.S. Supreme Court Justice Amy Coney Barrett denied a separate request by the Wisconsin Institute for Law and Liberty, working on behalf of a taxpayer’s association, to pause the program.

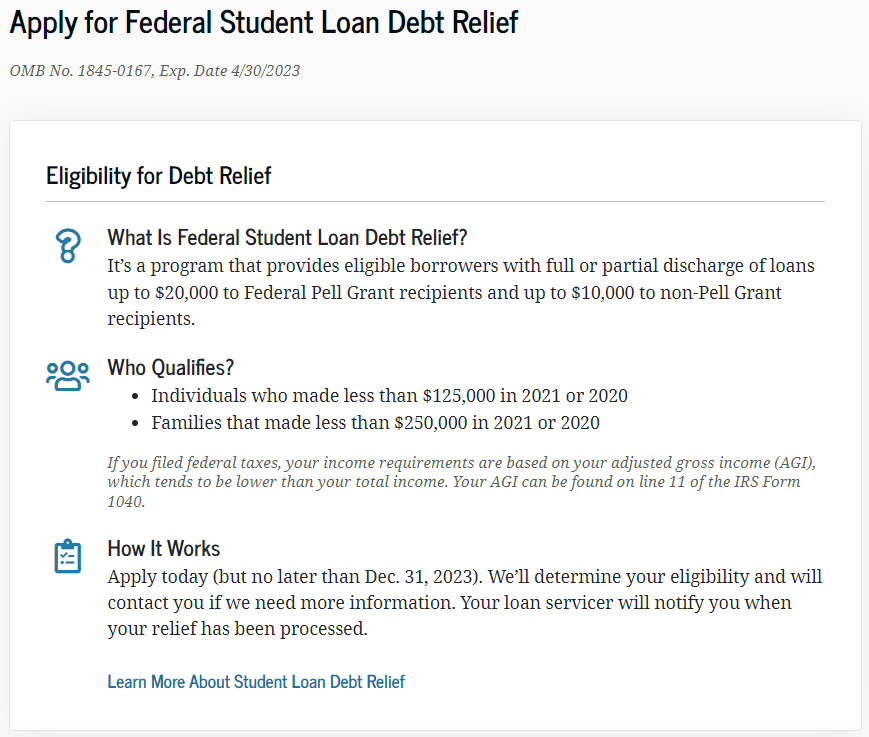

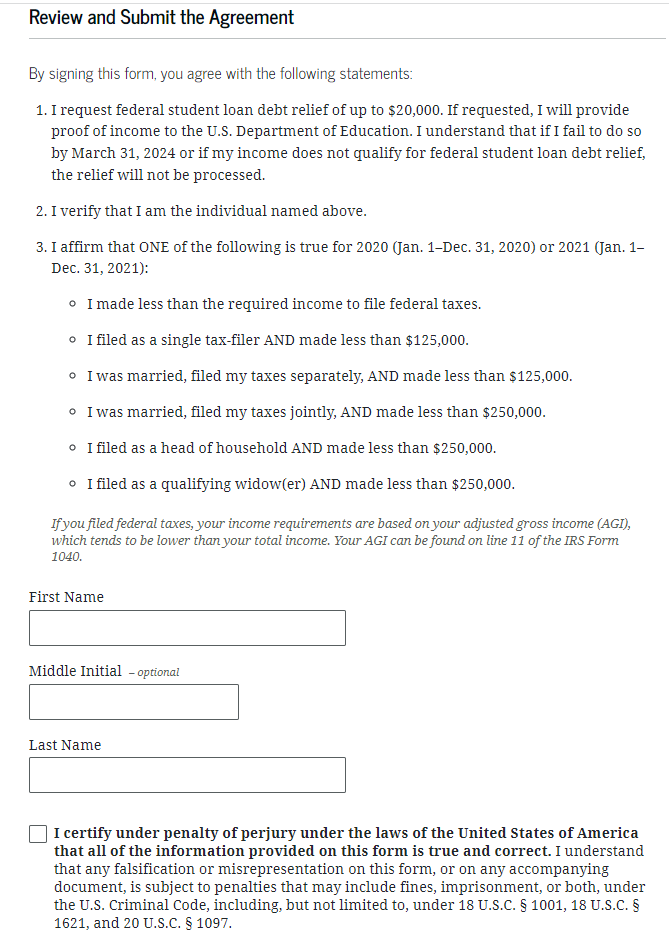

President Biden’s loan relief plan would discharge up to $10,000 in federal student debt for borrowers who earn up to $125,000 annually, or up to $250,000 for married couples. Borrowers who received Pell Grants are eligible for an additional $10,000 in forgiveness. Borrowers can apply until the end of 2025.

Biden hopes of it being processed before a pause on student loan payments ends Dec. 31.

CALL TO FIND OUT

833-782-7133

Following an abrupt change to eligibility rules in response to legal challenges, only government-held federal student loans are eligible for the student loan forgiveness relief. Commercially-held FFELP loans, which originally could qualify if consolidated, are no longer eligible as of September 29.

The application for the student loan debt relief program is still available. borrowers can visit studentloan.gov to apply. Applications will be submitted however not processed.

The administration hops to resume the cancellation as early as Dec 31st

Updated – Dec 10th 2024

The day we have all been so patiently waiting on is finally here. President Joe Bidens promised federal student loan forgiveness program application is finally ready to accept applicants.

The Biden administration discloses that this application is what they are calling a “Beta Version” of the application. All Americans seeking student loan debt relief can apply for the student loan cancellation. But must understand their application will be used for the purposes of improving the the process and application for future applicates.

In August, President Joe Biden announced his decision to cancel up to $10,000 in student loan debt for individuals making less than $125,000 a year or as much as $20,000 for eligible borrowers who were also Pell Grant recipients.

Individuals that apply for the debt cancellation in this “Beta” period will be emailed a confirmation that the application was received. However the debt relief application will not be processed until the formal application and site is released.

Borrowers that apply during this prelaunch will not need to reapply or resubmit there applications once the real site is launched. This testing period will allow the Dept of Education to pin point and resolve any bugs or issues to the site in real time. and monitor the functionality of the application and website.

Borrowers must have federally held student loans to qualify. In addition to federal Direct Loans used to pay for an undergraduate degree, federal PLUS loans borrowed by graduate students and parents may also be eligible if the borrower meets the income requirements.

Individuals with loans guaranteed by the federal government however are held by private lenders will not qualify as of right now. Programs like the Federal Family Education Loan program and Federal Perkins Loan program are also excluded from the forgiveness. These individuals would have needed to consolidate those loans into a Direct Loan by September 29th.

Borrowers who made less than $125,000 in 2023 or 2024 and married couples or heads of households that earned lower than $250,000 annually in those years are eligible for up to $10,000 of their federal student loan debt forgiven. The income elements are determined by the adjusted gross incomes.

Here is a preview of the application. This is no cost for the application. However paid services are available for assistance and guidance. For assistance from a student loan specialist click here.

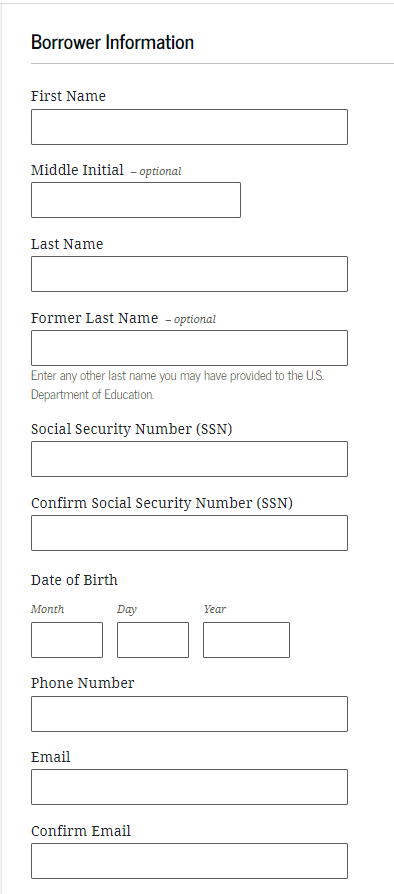

The application will begin with a brief description of who qualifies based on their income. followed by how the application process will work.

Below that you will see a link providing you with the option to learn more. This will be followed by an information form in which you will have to fully complete. and ends with an electronic signature of your fill name and an acceptance of the disclosure statement.

Once you complete that. will then need to hit the submit button.

Where professional may be needed is after this initial process. The Government informs us that individuals seeking the forgiveness. May be required to provide additional documents as well as other forms of verification.

After submitting the application once the website officially launches, most qualifying borrowers are expected to receive debt relief within weeks.

One program we can see with the process already. is that borrowers are not informed if the are eligible once they complete the application immediately. Leaving may feeling like they are approved, when in fact they may not. Borrowers will not be notified of this unfortune news until months later. This will leave borrowers feeling like they wasted their time when they could have used that time to investigate and seek other programs and help.

Because of this, we encourage borrowers to contact a student loan company and have them review your loans and help you to find out if your loans will qualify. A professional student loan company can assist in determining if your student loans have a chance at getting the Biden forgiveness. And if chances are that your loans will not qualify. They in many causes can direct you to other programs that my still be able to provide you with some debt relief or cancellation.

The honeymoon for student repayment is approaching its end. The hard reality is that as good as this Biden student debt relief is. Many will not qualify and benefit. Those individuals will have to start back paying on there student loans at the end of December 2025.

Many will have student loan payments they cannot afford struggle to pay. Income based repayment option may be a solution.

Are you thinking about buying your first house or maybe you are seeking to get a loan to start your own business. Truly the list goes on, there are many goals you could have great interest. In Which, your credit report and credit score will end up being the determining factor in your approval or rejection process. Which is one reason we want to discuss consolidation and affects on credit.

Rental rates, insurance rates, automobile loans, home mortgage loans and even job placement all are subject to your credit report and credit score. With good credit, you will have a much better chance loan approvals and lower interest rate offers on many of these financial products with lenders, banks and financial institutions.

However, a low or bad credit score in most cases will result in much higher interest rates which will cause you to pay more for a product than its value. A low or bad credit score can result in bank penalties, cancellation charges, credit card rejections and loan application denials.

The question you and many others may be asking is: Does my student loan affect my credit score? And the answer is YES! your student loans are affecting your credit score in a variety of ways, many of which you may not have been aware of….

Student loans generally fall into the same category as automobile loans and home mortgage loans.

These kinds of loans are considered as installment loans. An installment loan typically starts with a balance that is paid back over time and has a set number of repayments for that time period.

NO, all installment loans are calculated and regarded in the same way on your FICO score, therefore the type of student loan you have does not have an impact on how the loan is evaluated.

Student loans do not have their own their own credit category system.

Is getting more student loans bad for my credit?

Getting more student loans is not ideally bad for your credit score but doing can have a negative impact on your credit report.

Your credit score and your credit report are not always regarded or evaluated the same way.

For example, you may have a 700 credit score, but your credit report may document a number of reported outstanding debts, unpaid balances and a not to impressive payment history.

For Example, Home mortgage lenders and banks evaluate your debt-to-income ratio. This process is used to compare your total monthly debt expenses to your total income.

When this ratio is calculated to be to high, stating that there is too much debt in relation to your income, chances are you will be turned down for your mortgage loan application.

So therefore, ultimately your student loans can affect your credit score, they have a greater impact on affecting your eligibility to take out other loans and establish a good credit report.

So we know that your student loans themselves does impact your credit, but what about the student loan payments?

Probably the most impactful aspect of student loans on your credit is your monthly payments. More specifically, if you are making your payments on time and in full, part or interest only. This is important to understand regarding consolidation and affects on credit.

Changes to your credit score can depend on many factors. Payment history represents 35% of your credit score. This is the most regarded part of your FICO score, by being late on a single payment can cause your credit score to fall.

For example:

Philip currently has a credit score of 670. If Phillip becomes just 30 days delinquent on lets say his student loan payments, his credit score could drop 50 to 90 points from that one account.

Carla, who has a great credit score of 790 could suffer even more than Philip. With a 30 day delinquency Carla’s score would drop by about 100 to 120 points.

Also, if your student loans enter into default or gets sold to a collection agency your credit score as well as your report will suffer an even greater negative impact, often taking your credit score from very good to very bad in an instant. Just another note on Consolidation and Affects on Credit. ‘popmake-{getitnow}’

Your student loans do not have to be a bruise to your credit, in fact it may be possible for your student loans to become a credit score improvement agent.

Let’s say your credit is not so good, you have paid on your student loans and as a result your credit score has encountered significant drops. You may want to consider refinancing or consolidating your student loans. When you consolidate your student loans a lender can payoff your delinquent student loans and give you a new loan.

The new loan will be somewhat of a new start, providing you a second chance to make your payments on time, build new credit history for your student loans and reduce your income-to-debt ratio, if your payments are eligible to be reduced.

Fine out if you can get total loan forgiveness!

833-782-7133

Now you that you have a better understanding on Consolidation and Affects on Credit. You can decide if consolidation is an option for you.

Most people know what a calculator is, but few are aware of the power of a Student Loan Refinance calculator.

Students or former students may be interested in our student loan refinancing calculator If they are interested in refinancing your student loan.

With our new state of the art calculators we can help student compare and discover the best student loan refinancing options for their person student loan needs.

Which is why use a student loan refinancing calculator is important to discuss.

CALL TO FIND OUT

833-782-7133

To get your student loan interest, add all of your interest rates and multiple them by the number of interests. This is will give you your “weighted average interest rate”

No. The calculator with provide you with estimates of your savings based on interest rates you put in the system. To find out what your refinancing rate will be, request a contact from a student loan consultant

Fine out if you can get total loan forgiveness!

833-782-7133

We all have goals in live, many of us the goal of going to college, get our degree and move on to the career of our dreams. Our desired hope is that by getting a degree we will be rewarded with better job opportunities and better wages. However, secondary education can be very expensive. With work, family and many other responsibilities dropping out and sometimes become the only option. Refinance Without A Degree will be at the core of our topic in this article.

We all have goals in live, many of us the goal of going to college, get our degree and move on to the career of our dreams. Our desired hope is that by getting a degree we will be rewarded with better job opportunities and better wages.

However, secondary education can be very expensive. With work, family and many other responsibilities dropping out and sometimes become the only option. Refinance Without A Degree will be at the core of our topic in this article.

Unfortunately, those who are forced to drop out for whatever the reason will still be required to make payments on their student loan debt.

Refinancing your student loans can help in this situation, but a refinance without a degree can be pretty canny

Refinancing your student loans can make student loan debt much more manageable. Student refinancing can help with interest rates, alternative repayment options and possibly the lowering of your monthly payments. With all these benefits together, you may be able to free up more of your income to better budge. And a less stress on your financial responsibilities

When it comes to refinancing private student loans without a degree challenges will present themselves. Most lenders for private and/or federal student loans that you look to refinance with a private lender like a bank usually require completion of your degree program to be qualified for refinancing of your student loans.

However, still are some lenders that will refinance a loan of a borrower that did not graduate. Typically, a person that qualifies for this may have a different application process to complete

Unlike attempting to refinance a student loan through a private lender, refinancing through a federal program is much more forgiving. People that refinance their loans with the federal government are not approved or rejected for the student loan refinance based on if they graduated, received their degree, did not graduate or did not receive their degree. So, refinance without a degree on federal terms is a better situation.

Private student loans are not eligible for federal student loan refinancing programs.

For a person that did not graduate but is stuck with the obligation of repayment of their student loans. Federal student loan refinancing may be a primary option if they have federal student loans.

Based on studies, non graduates have a more difficult time meeting the minimum payment initially issued by their servicer. This could be due to low income, unemployment or other factors. Federal student loan refinancing can help such a person with alternative repayment options, deferment programs, forbearance. And plans based on income.

Many non graduates finds these programs very beneficial during difficult times.

CALL TO FIND OUT

833-782-7133

If you have federal student loans, you will usually enter a standard 180 month repayment 6 months after you leave school, whether you graduated or dropped out early. However, if your payments are too large for you to handle, you may be eligible for an income-driven repayment plan.

Income-driven repayment plans:

With each of these options your monthly loan payment is capped at a percentage of your discretionary income, and your repayment term is extended. That can dramatically reduce your payments, freeing up more money in your budget for your essentials.

Deferment gives a borrower the ability to stop their student loan payments for up to a full year at a time. Usually, a borrower is reward up to 4 deferments. Generally a person would seek to apply for a deferment if they are unemployed and does not see employment coming in the foreseeable future. And, or experiencing severe financial hardship seemingly for an extended period of time. Moreover, in some cases depending on your student loan type, the federal government may cover your interest on the payments for you.

If you are a student that withdrew from your degree program or dropped out for reasons important to you and your family. Do your research to find out what you can qualify for. Refinancing your student loans may be a viable option for you. Presenting the possibility of more attractive interest rates, alternative income sensitive repayment options. And payment stopping options like forbearance or deferments.

Refinance without A degree is a possibility for sure, you just have to fine what situation is best for you.

Fine out if you can get total loan forgiveness!

833-782-7133

Most of us have at least a few major goals like having enough money for retirement, starting a new business or saving enough money for down payment on a new dream home. But more many of us at the top of that list sits the goal of paying off our student loans. In this article we are going to talk student loan grants.

Surprisingly, not many of us are aware or have little knowledge about the possibility of grants to accomplish this goal of paying off their student loans

Believe it or not, there are many grants for student loans that can be used to pay off your student loan debt.

We all are aware that grants exist but generally we associate them with the act of looking to access funds to accommodate payment to attend a college or university. However, grants are available for individuals that work in specific fields or industries.

These grants for student loan payoff can help soothe a great deal of pressure from paying student loans.

There are many directions you can take for seeking a grant for student loan payoffs. The U.S. Dept Of Health and Human Services of the federal government has many grant options.

You can also search for grants by state. Sometimes the state works independently from the federal government and offers their own federal programs for grants. The goal is to encourage grads to build their careers in certain fields with and areas of need in our country.

If you work for a non-profit organization in certain fields there are also options to help with dealing with your student loan debt.

Here is a list of student loan grant programs individuals can pursue for student loan payoffs.

To qualify you must be:

A licensed Registered Nurse (RN)

A Nurse Practitioner

Work in a nursing facility with a degree in nursing

To qualify, you have to less than 24 years of age or have been attending as at least a part-time student during the time of the parents death.

Grant is specific for dentist and physicians that are willing to practice in economically challenged areas of the state of Pennsylvania. Receivers of this grant can receive from $30,000 up to $100,000 to go toward the balance of theirs student loan debt

There must be a 2 year service agreement for practice in the state to qualify. Applications must be submitted by Dec

CALL TO FIND OUT

833-782-7133

Students that enter into the field of reproductive research can receive up to $35,000 a year to assist with student loan repayment under the Contraception and Infertility Research Repayment Program. This program was structured to encourage students to work in the reproductive research field

Receivers must commit to two years of research in contraception and infertility. Visit the website to apply

Students that seek a career in farming can receive up to $10,000 a year for up to 5 years to payoff their student loan debt if they attend a college or university in New York and agree to operate a farm in the state of New York for a minimum of 5 years.

Applicants must apply within two years of graduating from school and private and federal student loan borrowers are eligible for this grant. Applications will be available in Oct.

Grant is for individuals that are state public defenders or state prosecutors. If so you may be eligible for the john R. Student Loan Repayment Program. Receivers can receive $10,000 a year for up to six years to payoff their student loan debt

You must agree to work as a public defender or state prosecutor for a minimum of three years to apply for this grant. Additional qualifications may be required, visit your state agency website to find out more.

If you attend a college or university in North Dakota and got your degree in Science, Technology, Engineering or Mathematics you could qualify for the North Dakota Science, Technology, Engineering, and Mathematics (STEM) Student Loan Grant.

Many receivers of this grant have been able to save on thousands over the life of repayment of their student loans and finish paying off their student loans in rapid time.

To apply for the North Dakota Science, Technology, Engineering, and Mathematics (STEM) Student Loan Grant you can submit your application after May 1st.

Borrowers that work for the government or a non-profit but are qualified for any of the student loan grants, you may be eligible for Public Service Loan Forgiveness. With Public Service Loan Forgiveness, after ten years of service while making qualifying 120 payments on your federal student loans, the government will give you forgiveness on the remaining balance.

If you still find yourself not falling into any of the categories above and are having trouble making your monthly payments and your student loans are federal government student loans, then seek to look into income driven repayment plan programs.

These programs can be a tremendous help if you find that you do not qualify for student loan payoff grants or Public Service Loan Forgiveness.

Plans Include: Income Based Repayment, Income Contingent Repayment, Pay As You Earn, and Revised Pay As You Earn

And finally, if you can do not find that the alternative repayment plans are not an option you could consider student loan consolidation.

Student loan consolidation can help in many ways from lower interest rates, reduced monthly payments to better loan terms and single loan accounts to manage easier.

With student loan consolidation you can save a lot of money and if you still have a balance at the end of your student loan consolidation term, you could still receive loan forgiveness after 300 months.

Fine out if you can get total loan forgiveness!

833-782-7133

As mentioned there are many options a borrower can look into for student loan grants, forgiveness or repayment options. Some options offers help for both federal and private student loan borrowers alike.

Be sure to check with your state and visit your state website for more information on these student loan grants offers for student loan debt payoff.

For information on repaying student loans, check out our article on student loan forgiveness programs.

Copyright © 2026 GOV STUDENT LOAN SERVICE. All rights reserved.