DO YOU QUALIFY FOR STUDENT LOAN FORGIVENESS?

2025

Easy to qualify programs for student loan relief

…I made the call and walked away with my loans forgiven!

You Should Call

The Truth About Student Loan Default in 2025—and How to Avoid It

The Truth About Student Loan Default in 2025—and How to Avoid It

After a three-year pause on federal student loan payments during the pandemic, repayment resumed in late 2023. By 2025, millions of borrowers have already slipped back into default or delinquency. What’s worse? Many of them don’t even realize it.

Student loan default is more than just missing payments—it’s a financial disaster that can lead to wage garnishment, credit destruction, and government collection lawsuits. This guide breaks down the reality of student loan default in 2025, explains the consequences, and—most importantly—gives you clear steps to get out and stay out of default for good.

What Does “Default” Actually Mean?

A federal student loan is considered in default when you haven’t made a required payment for 270 days (about 9 months). For some private loans, default can happen even sooner—sometimes after just 90 days.

Once your loan enters default, it’s no longer managed by your regular servicer—it’s sent to the Department of Education’s collections unit, and recovery efforts begin.

By the Numbers: Default in 2025

Here’s a snapshot of the federal student loan default landscape in 2025:

7.2 million borrowers currently in default.

Over $130 billion in defaulted federal student loans.

24% increase in defaults since the end of the pandemic-era payment pause.

Disproportionate default rates among Black borrowers, first-generation students, and those who attended for-profit colleges.

🔗 Source: Student Loan Data Center – StudentAid.gov

Why Do Borrowers Default?

Contrary to the myth, most borrowers in default aren’t irresponsible. They’re often:

Low-income earners who can’t afford high payments.

Unaware of income-driven repayment plans like SAVE.

Misled or poorly serviced by loan servicers.

Victims of compounding interest that inflated their balances.

Default often happens because the system is confusing, predatory, and designed for profit, not support.

What Happens When You Default?

Default isn’t just a slap on the wrist—it’s a hammer. Here’s what can happen:

❌ Wage Garnishment

The federal government can take up to 15% of your paycheck without a court order.

❌ Tax Refund Seizure

Expect to lose your entire tax refund, including the Earned Income Credit.

❌ Credit Score Drop

Default can lower your credit score by 100–150 points, impacting your ability to rent, buy a car, or qualify for credit.

❌ Federal Benefits Seized

In some cases, Social Security and disability payments may be offset.

❌ Loss of Eligibility

You lose access to IDR plans, new financial aid, and federal benefits until you fix the default.

How to Get Out of Student Loan Default in 2025

Here’s the good news: you can fix this, and thanks to recent programs, it’s easier than ever before.

✅ 1. The Fresh Start Program (Extended to 2025)

The Fresh Start initiative, launched in 2022 and extended through 2025, allows borrowers in default to quickly regain good standing with minimal effort.

Benefits of Fresh Start:

Instant removal of default status

Restored access to IDR and PSLF

Stops wage garnishment and collections

No need to make a lump-sum payment

How to Apply:

Call your assigned Default Resolution Group (DRG)

Opt in and begin repayment on a qualified plan

🔗 Internal Resource: How to Use Fresh Start to Escape Default

✅ 2. Loan Rehabilitation

Loan rehabilitation is another option—but it’s more time-consuming. Here’s how it works:

Make 9 on-time monthly payments (as low as $5–$50 depending on income).

After the 9th payment, your loan is removed from default.

Default status is deleted from your credit report.

Note: You can only use rehabilitation once per loan.

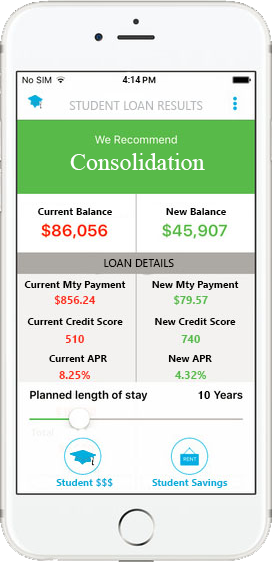

✅ 3. Loan Consolidation

You can also consolidate your defaulted loan into a new Direct Consolidation Loan, which brings it back into good standing instantly. But be careful:

Only works once.

Must agree to enter an IDR plan post-consolidation.

Collection costs may be added to your balance.

Comparing Fresh Start vs. Rehab vs. Consolidation

| Option | Speed | Credit Repair | Payment Flexibility | Best For |

|---|---|---|---|---|

| Fresh Start | Fastest | No | IDR available | Most borrowers in recent default |

| Rehabilitation | 9 months | Yes (removes default) | Low payments possible | Long-term credit recovery |

| Consolidation | Immediate | No | IDR available | Borrowers who can’t wait |

How to Avoid Default in the First Place

The best fix? Avoiding default altogether. Here’s how:

✔ Enroll in an Income-Driven Repayment Plan

SAVE Plan can reduce your payment to as low as $0/month.

Prevents interest growth and guarantees progress toward forgiveness.

🔗 Enroll in SAVE Plan

🔗 SAVE Plan Overview – StudentLoan-Gov.com

✔ Sign Up for Auto-Debit

Avoid missed payments and often qualify for a 0.25% interest rate reduction.

✔ Update Income Every Year

Re-certify on time so your monthly payment stays accurate. If your income drops, update early to lower your bill.

✔ Know Your Loan Type

FFEL and Perkins loans aren’t eligible for all IDR programs. Consolidate to access better plans and forgiveness.

What Happens If You Ignore Default?

If you ignore a default, the consequences don’t go away—they get worse:

You’ll pay thousands more in collection fees.

Legal action can be taken in court.

You’ll lose years of progress toward forgiveness.

Default status stays on your credit report for up to 7 years.

Who Is Most at Risk in 2025?

Unfortunately, the same groups continue to bear the brunt:

Borrowers with no degree

Single parents

Black and Hispanic borrowers

Attendees of closed or for-profit colleges

Older borrowers nearing retirement

If you’re in one of these groups, early enrollment in IDR or Fresh Start is critical.

Final Thoughts: Default Isn’t the End—But It Must Be the Turning Point

Student loan default is not a life sentence—but it is a serious financial red flag. The system might feel rigged, and the odds unfair, but in 2025, you have more tools and options than ever before to get back on track.

If you’re behind on payments, take action now. Avoid collections. Stop the interest. Protect your credit. Your financial future is still within reach—you just have to make the move.

Helpful Resources:

WANT YOUR LOANS FORGIVEN?

CALL NOW

833-782-7133

Need your monthly payments reduced?

Fine out if you can get total loan forgiveness!

833-782-7133

Other Related Articles

Student Loans 2025

The Trump Presidency

& it’s impact on:

- Student loan forgiveness

- Government loan programs

- Student repayment options

Recent Posts

Archives

Categories

Meta

GOV Student Loan Service student loan refinancing program can save you major time and money and we can prove it!

Hands Down

Recent Comments